Fintech conquering Belgium – the right UX is the engine for banking growth – part 1

Since 2010, the Belgian Fintech segment has been developing steadily, with the first players focusing on alternative financial solutions such as crowdfunding. However, the last few years have brought changes, the end of the decade saw the rise of payment solutions on the Fintech scene. This includes retail payment platforms, but the bulk of the market is focused on business-to-business payment services, such as professional foreign exchange payments for small and medium-sized enterprises (SMEs).

In the aftermath of Brexit, some well-known UK payment services providers (MoneyGram, TransferWise, Ebury and WorldRemit) have chosen Brussels as a base in order to continue serving the continent. Their arrival has contributed greatly to the maturation of the sector. This trend is becoming more and more prominent in the Belgian Fintech world, even following Great Britain’s departure from the European Union.

The main reason why international investors choose Belgium as a base to conquer the continent is that the Belgian regulatory authority is not only technically equipped, but also facilitates market entry by accepting licence applications in English. Belgium’s central location between the two largest economies in the European Union and its highly skilled and multilingual workforce also play a role. The latter also represents an interesting test market for financial products. As a result, a vibrant scene has developed in the country, coinciding with the expansion of UX agencies.

This article presents the key players in the Benelux Fintech segment from a user experience perspective, be it old incumbent service providers or young players that have only recently been established. It shows which age groups, services and technologies the market is moving towards to, and reveals that in certain areas and along certain interests, cooperation between banks seeking to transition from the old world and Fintech companies representing modernity is seen as more rewarding than rivalry.

KBC Belgium

Founded in 1935 as Kredietbank and known as KBC Group since 2005, this Belgian-rooted financial institution is the 15th largest bank in Europe based on market capitalisation. It has 12 million clients worldwide, with its main focus on the Central and Eastern European market, where almost 8 million clients use its services. The company, which focuses mainly on private individuals and small and medium-sized enterprises, generated net profits of around 2.5 billion Euros in 2019. It was voted Belgium’s best bank for the sixth year in a row.

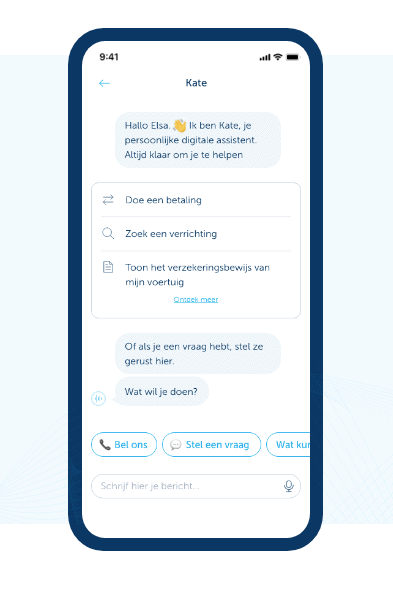

This artificial intelligence will convince even the Kate sceptics

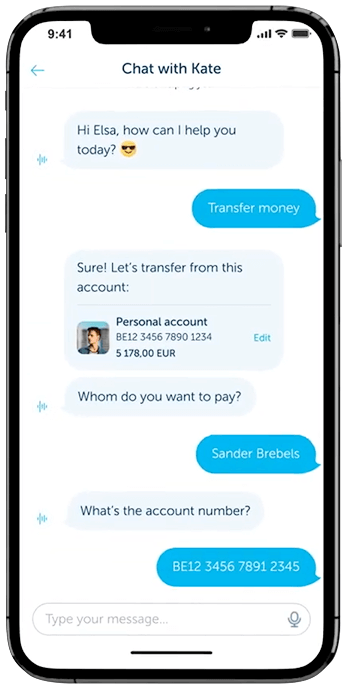

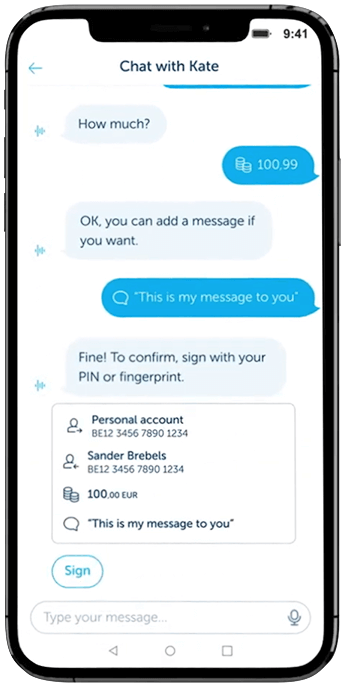

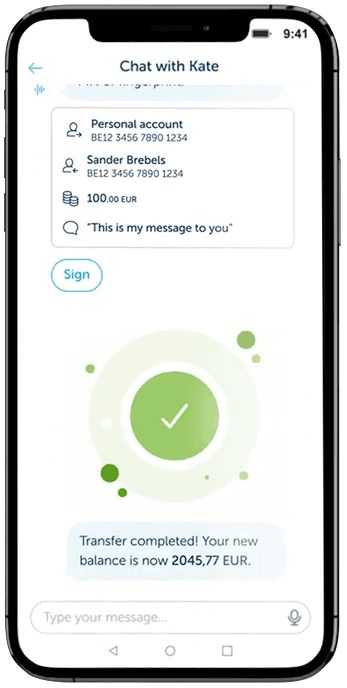

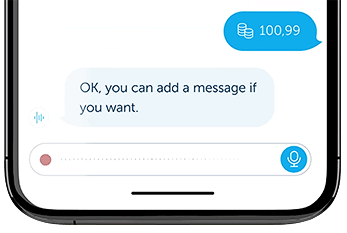

Kate became available to KBC’s private clientele at the end of November 2020. The digital assistant offers a personalised client experience and financial solutions that are relevant to the clients. It is a voice-controlled but also chat-enabled smartphone application that not only helps users organise their banking, but also retrieves their personal documents, provides investment advice and can even be used to buy and pay for train tickets. Its name is an acronym, short for KBC Assistant To Ease, referring to the concept of making life easier for clients.

Anyone establishing contact with the AI for the first time will have the option to choose the ‘advanced Kate’ option. This gives you proactive, personalised solutions, through which you can save time and money. Among other things, the digital assistant can help KBC clients save money on their electricity bill or warn them of potential storm damage.

While the digital assistant is highly effective within the financial framework provided, and statistically understands 90 percent of the questions asked, it is not always able to offer an immediate solution to inquiring clients. That is why KBC cannot just sit back and relax: the development and improvement of the efficiency of the service is ongoing. In around 12 percent of cases, Kate directs users to a bank employee working at KBC Live, therefore clients are not left to their own devices even if the artificial intelligence is unable to assist them.

In order to minimise the number of such situations, each day a team examines the questions that the digital assistant was unable to answer that day. Following the analysis, they make changes to Kate’s operations, so that the next day the artificial intelligence is up and running using what it has learned, to the greater satisfaction of clients and the investors and owners of the financial institution, who are constantly working to cut costs.

Successful implementation

KBC Mobile users have more than half a year of experience behind them. According to the financial institution, the results of the first six months are encouraging. Nearly half of KBC Mobile’s 1.6 million user base, has shown interest in the digital assistant: almost 800,000 individual clients clicked on or used Kate at least once during this period. This resulted in nearly 2.4 million conversations over the six months, roughly 30 percent of which resulted in additional activity (transactions, subscriptions to services, etc.). The survey found that the majority of clients are already using the artificial intelligence to access KBC Live directly.

Before the marketing campaign even started, nearly 42,000 clients agreed to try the ‘advanced Kate’ client experience. However, since the campaign launched in May 2021, interest in it has picked up significantly: according to the statistics of the financial institution, around 60 percent of the users contacted, accepted the invitation to try the option. This user base then received nearly 28,000 proactive notifications in less than a month, of which around a quarter were accepted, i.e. proved to be useful for the stakeholders.

During its operation, Kate sends personalised messages and Push messages to offer functions that can make the user’s life easier. There are two ways of communicating with her: the user can write or even say what they want and Kate will take care of everything. As voice communication is also available in the solution, the aim, in addition to providing a highly accessible interface, is to make the conversation itself and its wording easily understandable. It is clear that the developers of the application have tried to avoid banking jargon and for the system to communicate in a simple and understandable manner: always be able to offer the client a solution, If Kate is unable to assist, the client is redirected to KBC Live, where human advisors are available for them.

New investor group: targeting young people with little money

While KBC Kate is one of the most important Fintech developments of the Benelux financial institution, it is not the only one. During 2020, another important event happened in the bank’s life: it spun off its wealthtech business into a new startup. The declared aim of EveryoneINVESTED is to increase the willingness to invest: it promises to make the process less stressful and make investing more attractive to younger people.

The bank has thus opened up to new clients through B2B (business to business) tools over the past year, but opportunities are also available to its existing client base. However, these are not offered directly to consumers but to asset management companies by KBC Belgium’s start-up. Asset managers have at their fingertips tools such as “The Profiler”, which will allow them to create personalised risk profiles almost to the extreme to reveal the rational and emotional preferences of prospective investors. “The Matcher” helps to match third-party portfolios, and “The Decoder” makes it easier to understand the past history of different financial funds.

EveryoneINVESTED focuses on younger, less affluent investors with the help of behavioural technologies and the promise of better investment decisions. Wealth management service providers using the startup’s Fintech developments can build a more dynamic and loyal customer base through the B2B toolkit. Initial feedback has confirmed this claim: More than 10,000 young investors have been attracted, 11% of whom spontaneously re-invested without any further persuasion techniques during the first six months of participation in the programme.

KBC, K’ching: UX design for a young target group

How to revolutionise banking services for teenagers?

How can a traditional bank stay profitable in a highly regulated and fast changing market environment? How to attract the youngest digital natives and tomorrow’s spenders? KBC has decided to design a banking app tailored to the banking needs of 12-24 years old and create the KBC K’Ching app, which targets a predominantly young user group. Their solution, a smartphone messaging and chatbot app, was the first of its kind in Europe.

Banking app tailored to the needs of 12-24 year olds

The first generation of true digital natives prefer to use their smartphones for almost everything, be it shopping, playing games, sending emails or any kind of communication. It is natural for them to use it for banking. However, while on most online platforms they encounter simple processes when they want to bank – also on their mobile phones – open a current account or a savings account, the same teenagers are faced with complex solutions compared to other platforms. They are confronted with seemingly unnecessarily complicated administration, financial jargon and ‘exotic’ insurance products that they see no use for. Meanwhile, they would like online banking services, user-friendly solutions and simpler interfaces, but banking solutions, including KBC’s offers, are too complex for their needs and do not meet their expectations.

In response to this problem, KBC has created a solution called KBC K’Ching.

This is how it was created

They first created a prototype concept for the app in 2015 using the design sprint methodology developed by Google Ventures.

It was tested with potential users and they subsequently worked with this initial prototype in agile development. During this time, the designers worked with developers and business stakeholders to refine the default visual theme, chosen tone of voice and user experience. Throughout the design process, they regularly consulted with members of the young community representing KBC’s target audience. This helped the designers (Internet Architect) to be confident that the application would meet the needs of the target group.

In fact, according to Tim Wouters, researcher at Internet Architect, these regular consultations with members of KBC’s young target group helped them to be sure that the application they were developing would meet the needs of the target group. The app was available for download from iOS and Google Play from the end of September 2016, and the number of downloads reached a record within a short period of time.

Simple and conversational interface

Since more than 60 percent of smartphone usage is spent hanging out on social networks and messaging there, KBC’s solution basically follows the same steps as on these platforms. They’ve also simplified what they could.

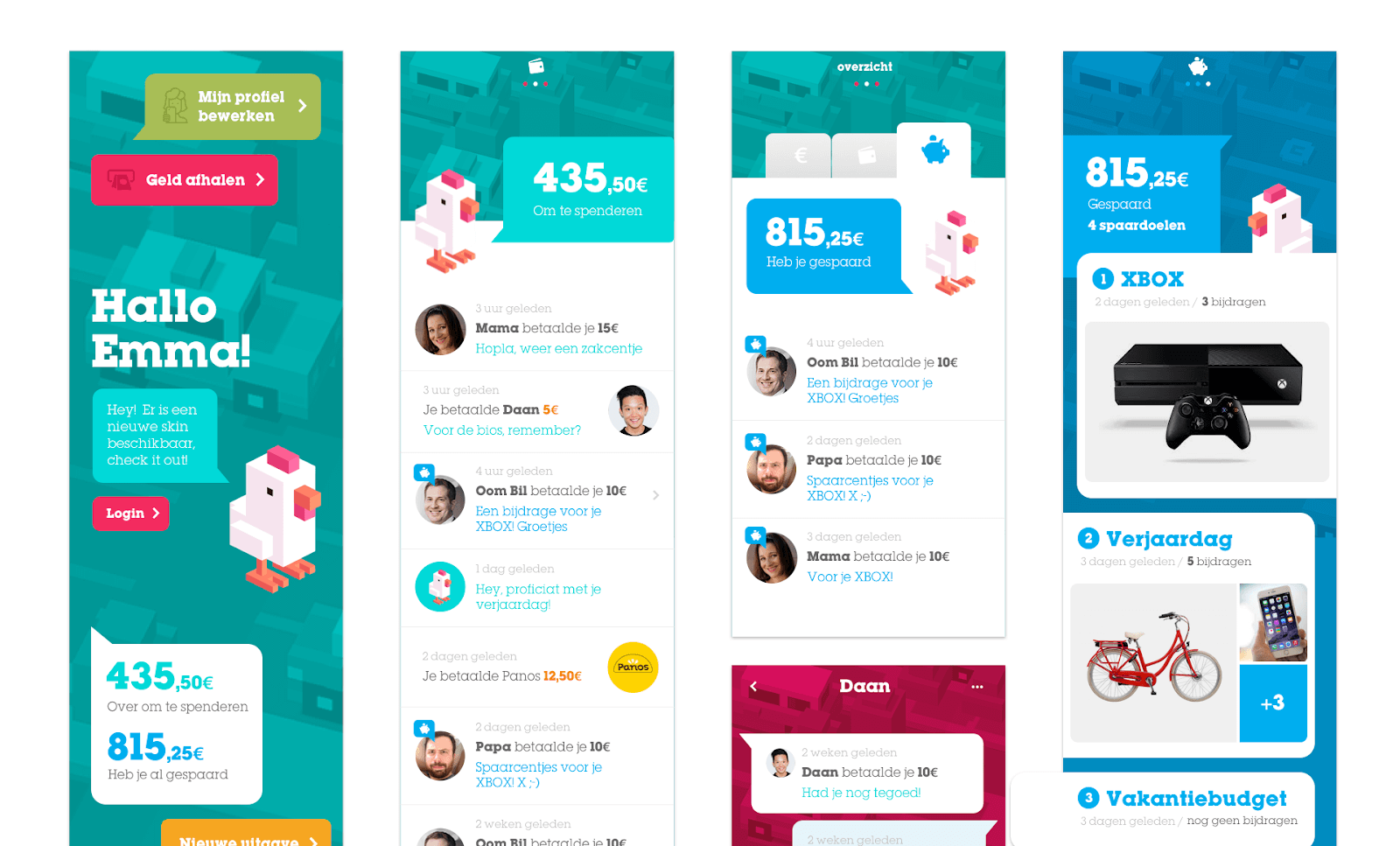

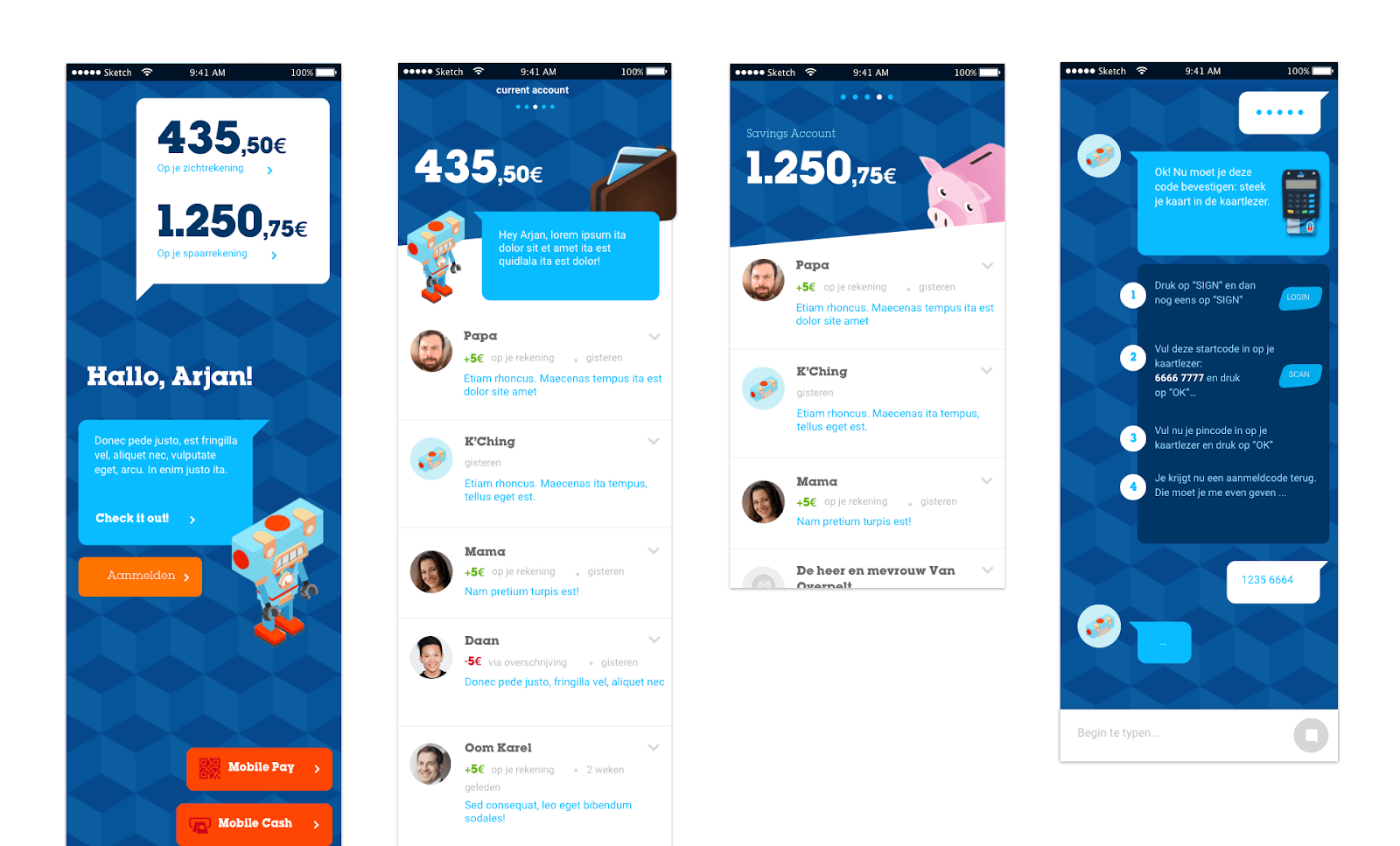

A very simple interface has been developed: young users only have to keep an eye on two wallets: cash and savings. What’s more, the entire registration and login process has been simplified to a single screen.

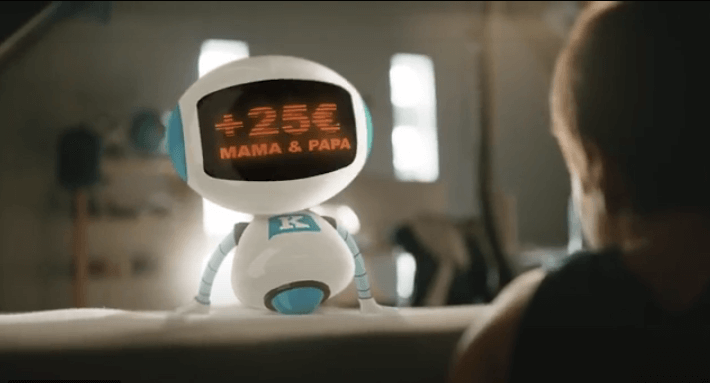

A customisable personal chatbot, K’Ching, guides the user through the process and offers advice when needed. All in a direct, conversational tone, teaching the younger generation responsible financial planning.

Finance = Conversation

The UX concept of the KBC app approaches finance as a simple conversation, and users can see past transactions as a chat history of messaging apps. Everything is simple, accessible and fun.

The value of basing the entire design and development on research and engaging with the target group throughout the process is demonstrated by KBC K’Ching’s popularity amongst young people: 80 percent of current users are aged 12-24, and two-thirds are minors.

Open thinking, continuous research and target audience engagement were therefore needed to create such a truly pioneer application with an innovative UX, where the chatbot already has the foundations of artificial intelligence and intelligent interactions.

Much depends on the first Fintech experience

KBC has made significant developments both conceptually and technologically, By “disguising” artificial intelligence as human, better user experience is coupled with more cost-effective operations. And the first encounter with finance is facilitated by a very likeable character and a style closer to the youth mindset.

Both developments have the potential to increase user loyalty, i.e. to make the bank’s customers not just see the bank’s improvements as a service, but like and stick to them.

Dr. Csilla Herendy

Senior UX Researcher

Her field of research is online communication, visual, ergonomic and navigational issues on online interfaces. She is a guest lecturer and researcher of the University of Bologna, as well as a freelance senior usability researcher of Ergománia Ltd.

recommended

articles

Find out more about the topic

We like you;

get in touch

Let's make memorable things together.

Dear Ergo,

Bartók Béla street 39.

1114 Budapest

Visitor info

Share your opinion with us